IP Migration Patterns

Maybe the Tax Cuts and Jobs Act did bring home valuable intellectual property--and the dollars that come with it--after all? Some new data points in the fog.

Last month I asked, “Does the Tax System Need FDII?”

(That’s the generous tax deduction for foreign-derived intangible income, also known as FDII or “Fiddy.”)

The policy was enacted by the 2017 Tax Cuts and Jobs Act, as part of a new international tax system that includes both carrots and sticks to discourage profit-shifting and incentivize companies to keep valuable intellectual property at home–or at least to ensure the scale isn’t tilting the other way. Without an incentive to shift IP and its income to low-tax jurisdictions, U.S. companies would be more likely to keep it home and the tax base would be stronger, in theory.

Since then, an overall conventional wisdom has solidified that those incentives weren’t strong enough, or were too riddled with loopholes, to create a true paradigm shift. Many companies opted to keep their structures in place, even if that increased tax costs. Fears that the TCJA’s incentives could be short-lived should Democrats retake power prevailed for many companies. (When it comes to IP, the U.S. is like Hotel California, I heard one practitioner say– "except you can’t even check out.") Still, despite this, there were individual reports of conglomerates which opted to repatriate valuable intangibles.

Mostly, the data was a bit of a fog.

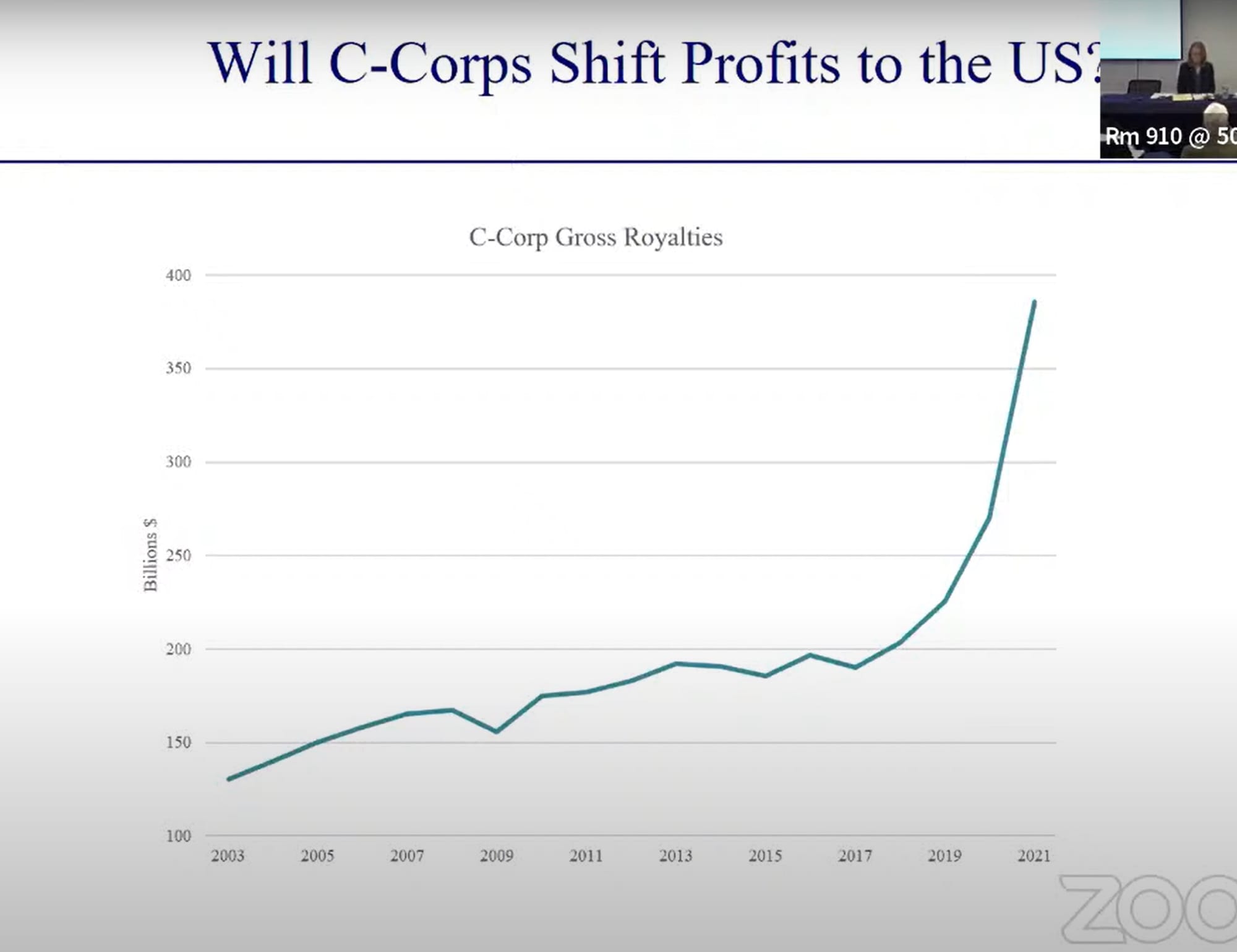

But since last month’s newsletter I’ve come across another data point that punctures a hole in that CW. During a presentation at a Georgetown University tax conference on April 5, Paul Landefeld, an economist with the Joint Committee on Taxation, noted that the U.S. has seen a sharp upsurge in corporate gross royalties since 2017. To get a sense of how sharp, take a look at his chart, using Internal Revenue Service statistics:

Royalties normally (though not always) are based on some type of IP, so this would seem to indicate some dramatic sea change in the incentives for intangibles location. It’s not like these companies had some explosion of new inventions in the past seven years. It’s circumstantial evidence that the TCJA’s international framework–and maybe FDII in particular–are creating the effects they intended.

It’s probably not all due to that, though. Landefeld noted that the date coincided with some other changes in the international tax system, including Ireland’s change in residency rules that made structures like the “Double Irish” impossible. Since that closed the Irish gateway to zero-tax Caribbean jurisdictions, it led to an increase in revenue sourced back to the U.S, as well as Ireland itself.

There was also the Organization for Economic Cooperation and Development’s 2015 Base Erosion and Profit Shifting project, the precursor to their Two-Pillar project and the 15% global minimum tax. The BEPS plan included an array of recommendations for countries to crack down on the kind of elaborate tax structures which companies had been using to shift IP profits. Even though in 2017 it may have been too soon for some of those policies to take effect, many companies got the message.

It’s a point that’s worth repeating–the OECD’s Pillar Two global minimum tax is entering a global tax system that’s already in a state of chaotic flux. This is why estimating the revenue it’s expected to bring in is close to impossible. And once Pillar Two has sunken in, it’s going to be a challenge to sort out its effects from those that had already been set in motion. For many, many years, we may not know what’s causing what.

To go back to the U.S., this reported surge in royalties raises the question–why then are there still companies that seem to be paying most of their tax offshore? Those companies may not have brought their IP home, but shouldn’t GILTI or other disincentives be making up the difference? I haven’t pored over the public filings to try to put all of this together, but what I suspect is that many companies would have seen a boost in U.S. taxable income due to IP repatriation, increased GILTI payments or changes in what their foreign subsidies pay to use domestically developed IP–but that’s getting eaten up by R&D credits, or the immediate deductions, expensing and net operating loss utilization that the TCJA put in place.

Many of those are timing differences, so the revenue could come back in later years. But, again, with so many factors at play, will it even be perceptible?

If FDII is working, that means it’s offsetting the effects of the patent boxes that countries in Europe and elsewhere have been using for decades to lure IP income to their shores. In fact, if all of these incentives are now canceling each other out, then it’s almost like they don’t exist at all–except that all IP income is being taxed at a lower rate. It’s worth asking whether that makes sense anymore, if tax competition for this type of income is neutralized. Why give the most profitable companies an extra tax cut?

Of course, no individual country would want to be the first to pull back their special IP regime and lose their competitive edge. The OECD is supposed to work around these “After you, Alphonse” problems and arrive at a consensus solution–and in a sense, that’s what Pillar Two does.

What they’re learning, though, is that it’s hard to stop intangible tax competition without increasing real, tangible tax competition–which shows no signs of slowing down. (Just look at Australia’s new green energy incentives, a response to the enormous incentives in the Inflation Reduction Act.)

Water will always find its way to the lowest point, and if you’re trying to stop it a better use of time is deciding where you want it to go.

DISCLAIMER: These views are the author's own, and do not reflect those of his current employer or any of its clients. Alex Parker is not an attorney or accountant, and none of this should be construed as tax advice.

A message from Exactera:

At Exactera, we believe that tax compliance is more than just obligatory documentation. Approached strategically, compliance can be an ongoing tool that reveals valuable insights about a business’ performance. Our AI-driven transfer pricing software, revolutionary income tax provision solution, and R&D tax credit services empower tax professionals to go beyond mere data gathering and number crunching. Our analytics home in on how a company’s tax position impacts the bottom line. Tax departments that embrace our technology become a value-add part of the business. At Exactera, we turn tax data into business intelligence. Unleash the power of compliance. See how at exactera.com

Thanks for reading! Don’t forget, you can sign up here for a paid Emperor Subscription, to get extra bonus content every week.

This Friday, I look at the history of Subpart F, the first controlled foreign corporation rule and one of the most powerful anti-abuse provisions in the world.

Subscribers can also access interviews with former OECD tax official Pascal Saint-Amans, Tax Foundation CEO Daniel Bunn, and M.I.T. professor Michelle Hanlon, as well as other content.

Again, this content will only be available to paid subscribers, and you can sign up here. The transactions are handled by Stripe, a safe and secure payment processing platform. (If anyone has any difficulties subscribing, please let me know.)

LITTLE CAESARS: NEWS BITES FROM THE PAST WEEK

- Once again, I have a news update I can't link to–the lack of any kind of update on the OECD's Pillar One Amount A text since the organization's self-imposed deadline of March 30. Three weeks have now passed and there aren't even crickets. Heck, it's been more than a month since the OECD's tax division has released anything. There have been some terse statements that work is ongoing but it looks like the OECD may not be able to keep up even the appearance of progress anymore. The remaining issues–reportedly, how to define digital services taxes, the treatment of withholding taxes, the strength of the Amount B provision, and whether to count Puerto Rico as a separate jurisdiction, among others–seem kind of small to hang up a project like this. I wonder if other countries are just fed up with the U.S. making demands while it looks unlikely to sign & ratify the agreement itself, something that former OECD tax chief Pascal Saint-Amans mentioned in his interview with me before the deadline passed. The next deadline on the timetable is June, when the OECD said the treaty would be ready for signing. If they blow past that, then all bets may be off, and we're onto the next phase–whatever that is.

- Speaking of Pillar One and digital services taxes, United States Trade Representative Katharine Tai testified earlier this month before both the House and Senate, addressing issues related to the Biden Administration's trade agenda. This includes what they plan to do about DSTs, the unilateral levies targeting revenue from digital activities, and which borth parties agree are unfair discriminatory taxes on American tech companies. With Pillar One, which is supposed to replace those, in limbo, the next step could be potential trade sanctions by the U.S. against countries which use them. That's something that the Trump Administration pursued, and which Biden has suspended–but not totally dropped. In her testimony, Tai said those sanctions have "remained part of our toolkit," and that they're exploring all options--but she added that the U.S. Treasury Department remains in the driver's seat on this issue. For now.

- Business associations are starting to push back on a proposed change in the United Nations model treaty, that would expand gross revenue taxation of some business services. The goal is simplification and moving away from physical presence standard–in a similar vein as the above-mentioned DSTs–but according to the National Foreign Trade Council it would "lead to double taxation and unreasonably increase compliance burdens for companies." And the U.S. Chamber of Commerce said sanctioning such taxes in a model treaty could lead to "a further proliferation of novel extraterritorial taxes that diverge in significant respects from traditional norms of international taxing jurisdiction." As the U.N. continues to explore taking on a greater role in the tax sphere, it's learning just how red-hot some of these issues are.

PUBLIC DOMAIN SUPERHERO OF THE WEEK

Every week, a new character from the Golden Age of Superheroes who's fallen out of use.

Captain Battle, premiering in Silver Streak Comics #10 in 1941. A battle-scarred World War I veteran, John Battle dedicated himself to stopping the next big global conflict. (The first comic was in May, seven months before Pearl Harbor.) He has no superpowers but as a gifted inventor he has powerful technology, such as the "Dissolvo Gun" and a jet-pack.

Contact the author at amparkerdc@gmail.com.